Clipperton releases today its paper “The Journey from Venture Capital to Private Equity: The 2026 Guide for Tech Startups.” Now in its third edition, this guide reflects two decades of advising Europe’s Tech sector through M&A, LBOs, and growth financing, combined with an ongoing dialogue with VC funds, PE sponsors, and founders who have completed the transition. It examines what 2026 has changed in the PE exit landscape, what funds are really looking for, and the concrete tools from KPI frameworks to an interactive VC-to-PE deal model – founders need to navigate a narrower, more selective market.

When we published the first edition of this report in 2023, a PE buyout was still widely seen by founders and VCs as a fallback option, a plan B for companies that couldn’t reach an IPO or a strategic trade sale. Three years and dozens of advised transactions later, that perception has fully reversed: PE is no longer a consolation prize; it has become the primary and most credible exit path for European VC-backed Tech companies.

📌 Some highlights from the 2026 report:

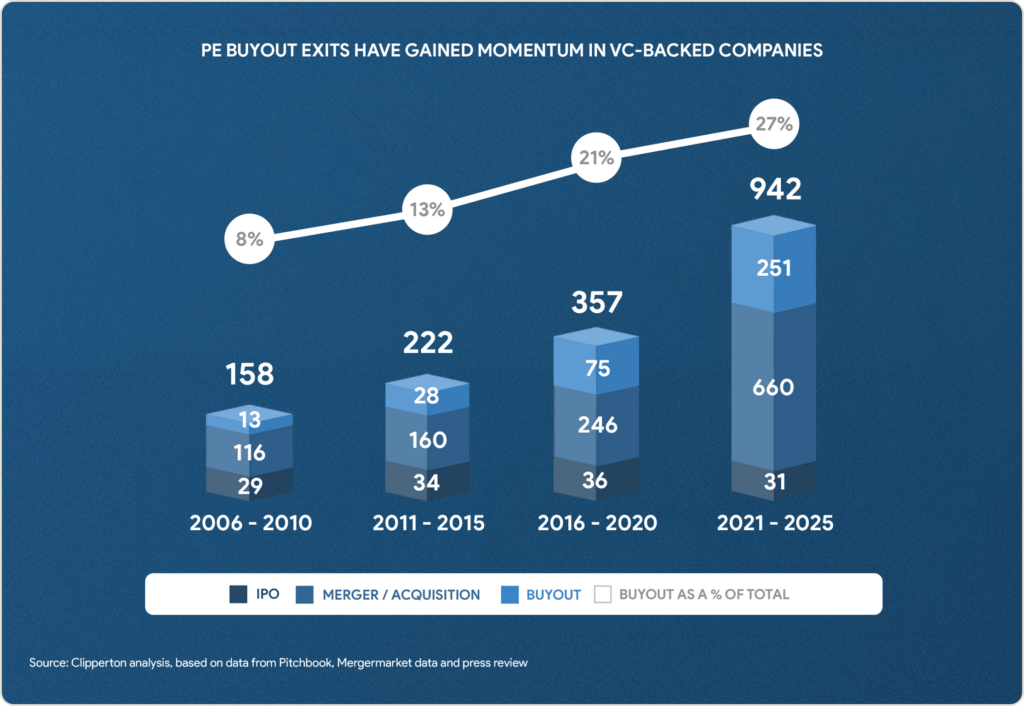

- PE buyouts represented 33% of VC-backed exits in Europe in 2025, up from 8% in 2006–2010 – and 82% of French software exits above €50m were PE-led. A structural rebalancing, not a passing trend.

- PE funds investing in Europe raised €107bn in H2 2024/H1 2025 – 3.7x the 2012 level. Dry powder is at record highs, and funds need to deploy it; VC-backed Tech remains one of the most attractive asset classes to do so.

- DPI pressure, not just strategic conviction, is now the primary driver of VC-to-PE activity. VC funds from the 2019–21 vintage boom are sitting on large unrealized portfolios, and LPs are demanding distributions. For many GPs, a PE exit is now the most credible path to return capital within 12–18 months.

- AI has become the decisive filter in how PE funds screen targets. Funds increasingly distinguish between software assets whose moat AI reinforces – systems of record, network-effect platforms, high-ROI SMB tools – and those exposed to commoditization, reshaping due diligence well beyond profitability metrics alone.

- The same PE deal can generate very different multiples for each stakeholder: a 3x deal-level multiple can translate into 5x or even 7x for management, once leverage, roll-over and the management package are factored in.

What’s covered in this report:

- The 2026 reset: the DPI reckoning, landmark deals, and the AI/SaaSpocalypse debate reshaping the exit conversation;

- Market context: the DNA of VC vs. PE investors, and the rise of private equity as a credible liquidity path;

- The build-up alternative: bolt-on strategies as an interesting alternative path for entrepreneurs and VC funds;

- What PE funds want in 2026: target profiles, the AI catalyst, and how leverage reshapes returns for each stakeholder;

- Preparing the transition: business plan execution, KPI tracking, deal structuring, and our outlook for the years ahead.

Fill out the form below to receive the report via email:

Authors: feel free to reach out to discuss these insights.

- Antoine Ganancia, Managing Partner

- Laurence de Rosamel, Partner

- William Poirson, Director

- Stéphane Valorge, Senior Partner – Head of Research

One of the most active M&A advisors in Europe for Tech buyouts